DOWNLOAD THE APP

Customer Services

Copyright © 2025 Desertcart Holdings Limited

DOWNLOAD THE APP

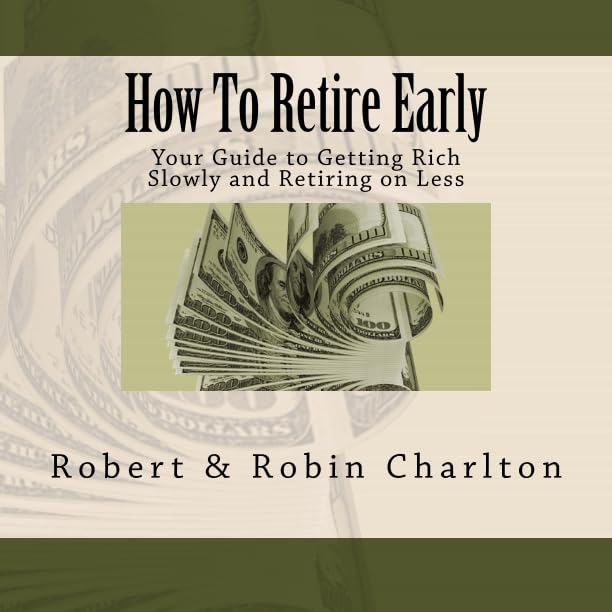

How To Retire Early: Your Guide to Getting Rich Slowly and Retiring on Less [Charlton, Robert, Charlton, Robin] on desertcart.com. *FREE* shipping on qualifying offers. How To Retire Early: Your Guide to Getting Rich Slowly and Retiring on Less Review: Planning for my early Retirement - I have been reading a lot of books lately on retirement planning. Really enjoyed this one. It is easy to read and has a lot of good information in it detailing exactly how Robert & Robin planned for, achieved their goal of early retirement, and how they are doing now after being retired for several years. I am still trying to get my wife to read the book so we will be on the same page in working for our goal of early retirement. We have already set the date that we plan to retire by and are implementing the plans to get there. We want to retire while we are still young enough to spend more time traveling and doing the other things that we don't seem to have time to do while working our 8 to 5 jobs. I only wish I would have had this book earlier so we could have planned for a much earlier retirement. The book discusses how to figure out how much money you will need to retire, how to safely build that nest egg, and how to live off of it through retirement. There is even a chapter discussing the very important topic of health care during retirement including some basic information regarding the Affordable Health Care Act. There is also a chapter with tips for travel during retirement. Robert and Robin apparently have traveled extensively since retiring. Looking at their website encourages us as we would like to do some traveling as well. If you dream of retiring early and possibly traveling, or just living a life of leisure this book could provide a good framework for planning to do just that. Review: and really enjoyed it. Easy to read - One of the first books on retirement I read, and really enjoyed it. Easy to read, and I liked that the authors laid out literally everything they did, with a lot of detail on their personal finances. Would recommend it to anyone starting to learn about retirement, even if you aren't planning on retiring early. However, one issue I had with the book is that the authors assume throughout the book that if you follow their example, you too can expect to retire in 15 years, maybe 20 if you have children. I suspect they may be greatly underestimating how important the timing of their investments was to their success - they started in the '90s, when the stock market was doing exceptionally well, and sold their house in 2006, at the peak of housing prices and just in time to avoid the housing crisis. As I recall, the authors acknowledge this only briefly somewhere in the middle of the book.

| Best Sellers Rank | #429,811 in Books ( See Top 100 in Books ) #282 in Retirement Planning (Books) #1,324 in Investing (Books) |

| Customer Reviews | 4.6 4.6 out of 5 stars (387) |

| Dimensions | 8.5 x 0.57 x 8.5 inches |

| ISBN-10 | 1482653729 |

| ISBN-13 | 978-1482653724 |

| Item Weight | 1.21 pounds |

| Language | English |

| Print length | 252 pages |

| Publication date | March 21, 2013 |

| Publisher | CreateSpace Independent Publishing Platform |

K**.

Planning for my early Retirement

I have been reading a lot of books lately on retirement planning. Really enjoyed this one. It is easy to read and has a lot of good information in it detailing exactly how Robert & Robin planned for, achieved their goal of early retirement, and how they are doing now after being retired for several years. I am still trying to get my wife to read the book so we will be on the same page in working for our goal of early retirement. We have already set the date that we plan to retire by and are implementing the plans to get there. We want to retire while we are still young enough to spend more time traveling and doing the other things that we don't seem to have time to do while working our 8 to 5 jobs. I only wish I would have had this book earlier so we could have planned for a much earlier retirement. The book discusses how to figure out how much money you will need to retire, how to safely build that nest egg, and how to live off of it through retirement. There is even a chapter discussing the very important topic of health care during retirement including some basic information regarding the Affordable Health Care Act. There is also a chapter with tips for travel during retirement. Robert and Robin apparently have traveled extensively since retiring. Looking at their website encourages us as we would like to do some traveling as well. If you dream of retiring early and possibly traveling, or just living a life of leisure this book could provide a good framework for planning to do just that.

D**9

and really enjoyed it. Easy to read

One of the first books on retirement I read, and really enjoyed it. Easy to read, and I liked that the authors laid out literally everything they did, with a lot of detail on their personal finances. Would recommend it to anyone starting to learn about retirement, even if you aren't planning on retiring early. However, one issue I had with the book is that the authors assume throughout the book that if you follow their example, you too can expect to retire in 15 years, maybe 20 if you have children. I suspect they may be greatly underestimating how important the timing of their investments was to their success - they started in the '90s, when the stock market was doing exceptionally well, and sold their house in 2006, at the peak of housing prices and just in time to avoid the housing crisis. As I recall, the authors acknowledge this only briefly somewhere in the middle of the book.

B**E

Inspiring

I am a financial advisor and I enjoyed this book very much. I am planning on adding the print version of this to the lending library I keep for clients- this is saying something- I read and discard probably 6 or 7 financial books to every one I keep to lend. My husband and I are getting close to retirement too and I think this book will be helpful in convincing my husband that it really is okay to retire now- or soon anyway. The Charlton's philsosphy about money and dedication to saving is inspiring, and I wish this could be taught in schools. Many people do not have the dedication to do this but some simply don't know its possible. I wasn't a fan of all of the investment advice, but I concede that its very difficult to give investment advice in a book- the market is situational and clients are individuals after all! This book isn't really about investment advice though- its about saving to meet a goal and I did appreciate the Charltons telling what they DID, warts and all. I found the discussion on taxes in retirement very interesting. Overall I think this is a blueprint that could work for a lot of people. Our situation is different as we have 2 grade-school age children, but it won't be difficult to adjust the calculations for that. I wish they had covered a little more about how they allocated their spending AFTER retirement- I'm pretty good at the saving part, but accurately calculating how much I will need to travel and live in retirement is a little scary for me. Did they calculate correctly, underestimate? Did they forget to include anything in their calculations? I would be interested to know what percent of their income goes to trips and how much goes to daily living expenses. By the way, I wrote down my retirement date- it felt great!

T**R

Helped me get un-stuck and start my retirement planning

I found this book when searching online about how to retire early. I just had decided to try putting myself on the 10-year plan for retirement or semi-retirement, and wanted to know how to go about doing it. This book is laid out in a very clear and logical manner and explains how to plan for retirement in various scenarios...kids vs no kids, retiring in 10, 15 or 20 years, anticipated expenses in retirement...different ages at retirement, which determines how much of your portfolio should be in tax-advantaged accounts, how big your nest egg needs to be, etc, etc. In this book, I was always able to find an example applicable to my situation, which allowed me to come up with a clear plan. Until now, I had put off any sort of realistic planning for the future, including investing money, because of all of the uncertainty and conflicting information out there. I was paralyzed and just avoided the whole subject because it was ambiguous and “icky.” I’ve had this book less than a month, and I have set up investment accounts based on information I’ve read in it. Now I have a clear plan to follow going forward, while not obsessing about the stock market. Of course there is always uncertainty, but now I have a better understanding of the different variables and it is not as complicated as I once thought. If you are a beginning investor or someone who has avoided thinking about retirement planning because it was too overwhelming, I highly recommend this book!!!

K**N

One of the best Retirement Books Ever!

This is one of the best retirement books I've ever read (and I've read a lot of them). There is such practical and helpful retirement advice throughout the book. I also found the book really inspiring and it motivated me to retire two years earlier than anticipated at 55. Highly recommended!

T**I

Lovely book! Very practical stories from the authors. They motivated me to continue on a path I was already on. I got this book because they were very honest and straight forward in their approach. I enjoyed the invest in yourself option, that is something we easily overlook today!

M**T

A good book and a worthwhile read. As a Canadian, I wish some information had been provided for those of us about to FIRE north of the border.

A**R

Great book, the end chapters are very U.S focused, but overall a good read. The spikes in income that the authors had (good job!) can be a bit discouraging, because we have to earn so much more to make it where they did!

Trustpilot

2 weeks ago

1 month ago